Why Fabless Ate Semis

Hyperscalers show up twice in the ecosystem - and that’s the tell.

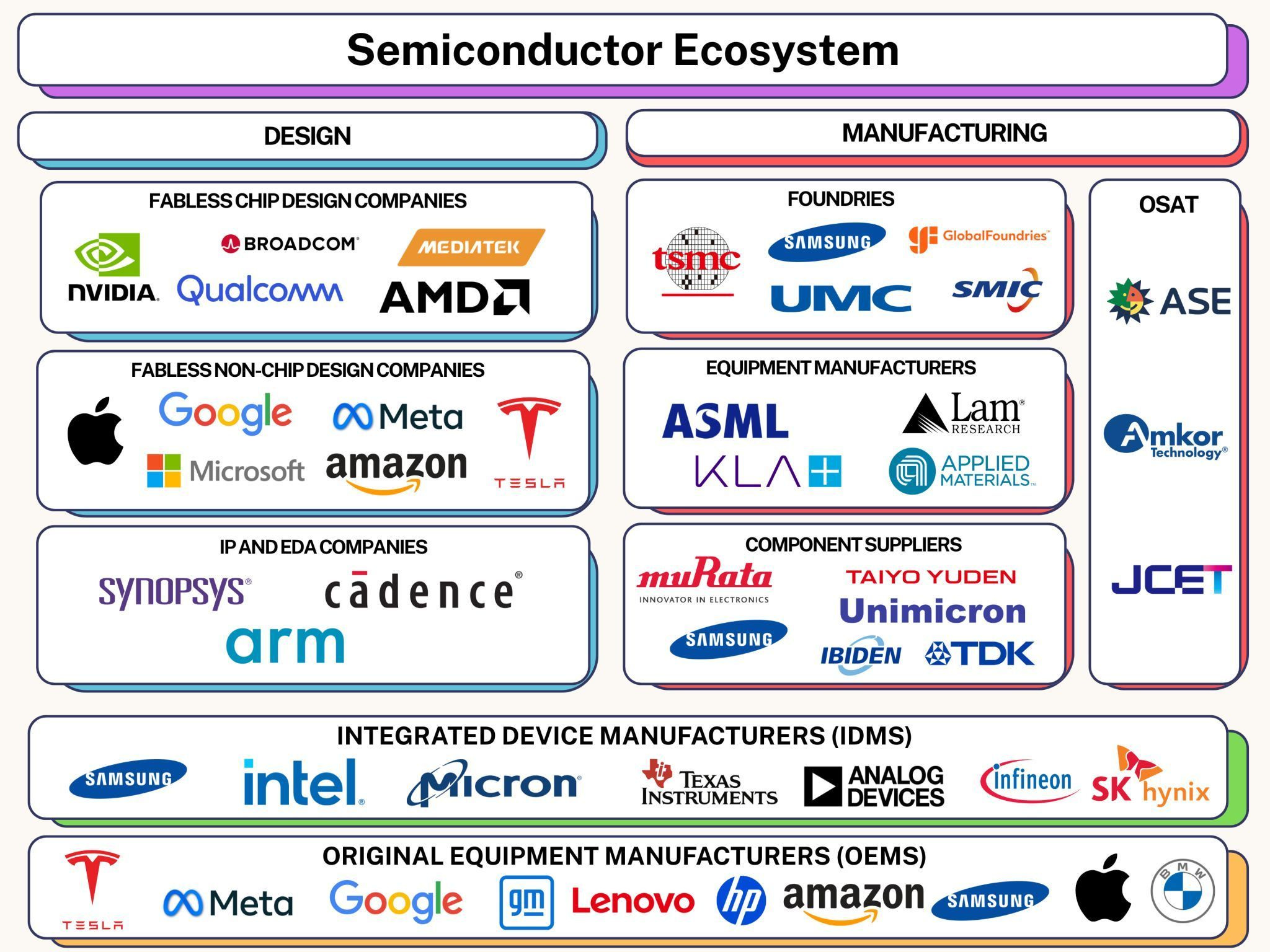

Looking closely at the ecosystem map shared on LinkedIn by Ali Kamaly recently, something is striking about this ecosystem you don’t see in many ecosystems: hyperscalers Google, Microsoft, Meta, and Amazon show up twice, once as fabless chip design companies, and once as OEM’s.

Why are they showing up twice? They play two distinct roles, and appear as:

Fabless system designers. At the top of the ecosystem, they define workloads, select architectures, and set specs.

OEMs/platform owners. At the bottom of the ecosystem (or the consumer end of the pipe) they ship and operate the end system.

That dual role changes everything. They’re still customers, but they’re no longer just customers. In short: they don’t just buy chips - they shape what gets built.

How Did We Get Here?

Why did hyperscalers moved into chip design. The “fabless takeover” story is driven by four forces in the industry:

1) Workload-specific performance beats general-purpose

General compute load has gotten heavier, and specialty chips have become increasingly viable. AI training/inference, recommender systems, video, search: the gains come from tailoring compute + memory + interconnect to their workloads. This drives economics, better performance per Watt, per dollar, and total utilization (the hidden killer metric in data centers).

2) The bottleneck is system-level, not chip-level

Once you’re at scale with these chips, and have scaled demand, the limiting factors become memory bandwidth, networking, power & cooling. Owning the silicon roadmap lets hyperscalers optimize the whole stack.

3) Supply chain power & allocation

Custom silicon is also a procurement weapon. If you’re running design in house, it slows down IP leakage. But it can also help secure better terms for purchase, and reduce dependency on IDM roadmaps.

4) Economic capture

If you operate at hyperscale, and you’re looking for a place to deploy capital, you don’t just want margin. You want rent capture via platform control (cloud services, hardware/software co-optimization).

Where is this heading?

Fabless Is Becoming System-Dominant—and Foundries Are Becoming Subordinate.

The center of gravity in semiconductors is shifting away from manufacturing leadership toward system ownership. Hyperscalers will increasingly define the workloads that matter - along with memory, interconnects, and packaging architectures.

In that world, foundries behave less like technology leaders and more like capacity providers, where how fast they deliver may matter more than abstract node leadership. Power accrues to those who control demand at scale, not necessarily to those with the most advanced process.

As a result, foundries compete on reliability, geopolitics, and allocation as much as on nanometers. This dynamic helps explain why companies like Apple, Google, and Amazon can punch far above their weight without owning fabs - and why future semiconductor winners may look more like platform companies than traditional chip manufacturers.